Image source: Getty Images

Building a second income may feel out of reach for anyone starting from scratch at 45. But with 20 years ahead until retirement, investors still have time to put compounding to work — and potentially build a £17,360 annual income stream in later life.

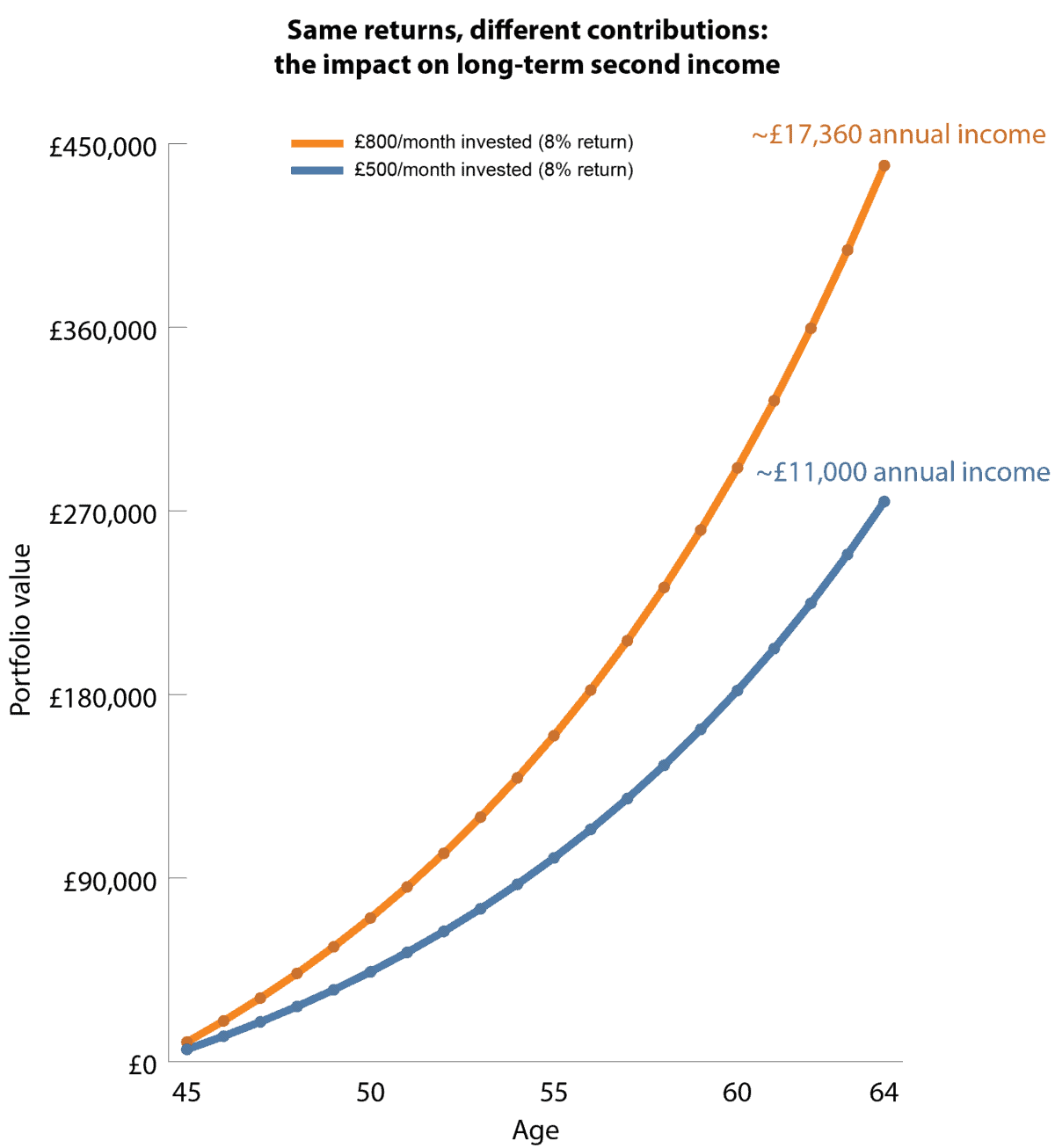

Starting later in life doesn’t mean building a second income is simply a case of investing more each month. While higher contributions can help, the real driver of long-term wealth is how long money is invested and how effectively it compounds over time.

Making up for lost time

Importantly, both scenarios in the chart below assume the same annual return of 8%. In other words, the rate of compounding is identical in each case.

Even with a 20-year horizon, those effects can still be powerful. The key is getting money into the market and allowing returns to build on themselves, rather than leaving cash on the sidelines.

The chart below isn’t just about contribution levels. Instead, it highlights how putting more money to work earlier — and keeping it invested — can significantly increase the income a portfolio is capable of generating over time.

Chart generated by author

The key takeaway is that both portfolios grow at the same rate. However, the higher monthly contribution simply results in a larger pool of capital for that same compounding effect to work on over time.

A steady income compounder

Headline-grabbing yields don’t come much higher than Legal & General (LSE: LGEN). With a forward dividend yield of around 8.2%, the appeal for income-focused investors is obvious. But the real attraction lies in the consistency of the cash generation behind it.

The group is not simply paying out a high dividend; it’s operating a business model built around long-term pension risk transfer, annuities, and asset management. That creates highly predictable, recurring cash flows that support both dividends and buybacks over time.

FY25 results reflected that resilience. Core operating earnings per share rose 9%, sitting at the top end of the firm’s long-term 6%-9% growth target range, while the Solvency II coverage ratio remained strong at 203%. Shareholder returns were further underpinned by a £1.2bn share buyback, funded largely through portfolio optimisation.

Looking ahead, structural demand in the UK retirement market remains a key driver. Defined contribution pensions are still expanding, and demand for annuity and pension risk transfer solutions is expected to remain strong over the long term. The company also retains visibility on a significant pipeline of potential deals, supporting medium-term income stability.

However, risks remain. As an asset-heavy insurer, it’s exposed to movements in bond markets and credit conditions. A sustained rise in defaults or a sharp deterioration in fixed income valuations could pressure both earnings and dividend capacity. Likewise, weaker equity markets could reduce assets under management and fee income.

Despite this, the core appeal remains unchanged: a high-yielding business with relatively visible cash generation, returning capital steadily through cycles rather than relying on short bursts of growth.

Bottom line

The chart above illustrates the power of compounding in building a second income over time. Legal & General operates on a similar principle internally: consistent cash generation is reinvested into shareholder returns, primarily through dividends and buybacks, allowing investors to benefit from compounding at both the portfolio and business level.