Image source: Getty Images

Diageo (LSE:DGE) has been dragging in my Stocks and Shares ISA for some time. And it’s not like it’s been a bad period for the wider market.

The FTSE 100 is up 78% in the last five years, but Diageo is down 56%. I haven’t owned it for all of that time, but it’s got me thinking of something Warren Buffett said.

What does Buffett say?

Warren Buffett is known for a few things. One is being willing to hold stocks for the long term and another is seeing low share prices as buying opportunities.

Despite this, Buffett also said the following:

“Should you find yourself in a chronically leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.”

In other words, the decision to never sell isn’t automatic. If a company has problems that can’t be fixed, it’s best not to wait around.

Diageo has certainly had issues recently. But the firm has brought in Sir Dave Lewis to try and get things back on track.

The new CEO has a plan and there are signs that things are moving in the right direction. The question, though, is whether there are better opportunities elsewhere.

Turnaround strategy

Diageo hasn’t become less competitive. It still has a huge distribution network along which it pushes category-leading products.

The trouble is with the categories themselves. Under its previous management, the firm focused on winning market share from beer and wine.

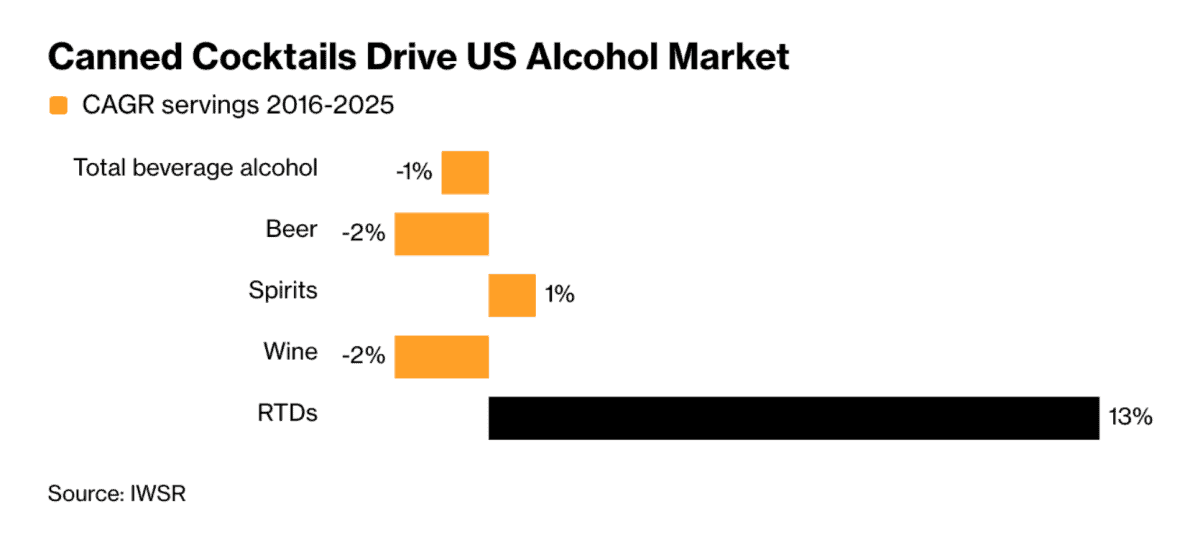

That, however, isn’t where the real action is. The latest data from the IWSR sets out clearly that where consumers are right now is the ready-to-drink (RTD) market:

So far, Diageo has been uncompetitive in that part of the market. But Dave Lewis intends to make this an area of focus for the company in the near future.

That’s where shareholders like me find ourselves. So is this a chronically leaking vessel, or a business that’ll be shipshape again before too long?

Will it work?

I think a lot of Diageo’s key strengths should translate well to the RTD market. It’s late to the cocktail party, but it brings a lot of brand heritage.

There is, however, a big risk and it’s one that I’m very wary of given my own experiences as an investor. Ever heard of Boston Beer?

In 2020 and 2021, hard seltzers were the big thing with consumers. And Boston Beer was extremely well-positioned to take advantage of this.

Yet that ended as quickly as it started. So the company was left with huge quantities of unusable inventory that it had to write down at a terrific cost.

My own investment in the firm ended badly some time ago. And it’s an object lesson in what can happen when consumer preferences change.

What should I do?

My instinct is to stick with my Diageo investment for the time being. Its product line-up and its distribution mean it’s not the same as Boston Beer.

The move into RTD products could be a lucrative one. But success isn’t guaranteed and consumer preferences can – and do – change.

I’m minded to stick with the stock for the time being. I will, however, be keeping a close eye on the next strategy update in August.