Image source: Getty Images

The first Berkshire Hathaway (NYSE:BRK.B) meeting without Warren Buffett felt different. Fundamentally though, not much has changed.

New CEO Greg Abel’s approach might be frustrating onlookers. But, as a shareholder, it was exactly what I wanted to hear.

Cash is… trash?

Berkshire’s cash reached around $380.2bn. And I sense that’s testing the patience of some investors. The S&P 500‘s up 27.96% in the last 12 months but Buffett’s firm has earned nothing like this on its excess cash reserves.

At the Annual Shareholder Meeting, Abel echoed the company’s recent view: it just doesn’t see opportunities right now.

Investors increasingly seem to be arguing for the firm to use its cash or return it to shareholders. But that isn’t what I want to hear. I don’t think Berkshire Hathaway’s a stock for most investors. But I also don’t see that as a bad thing.

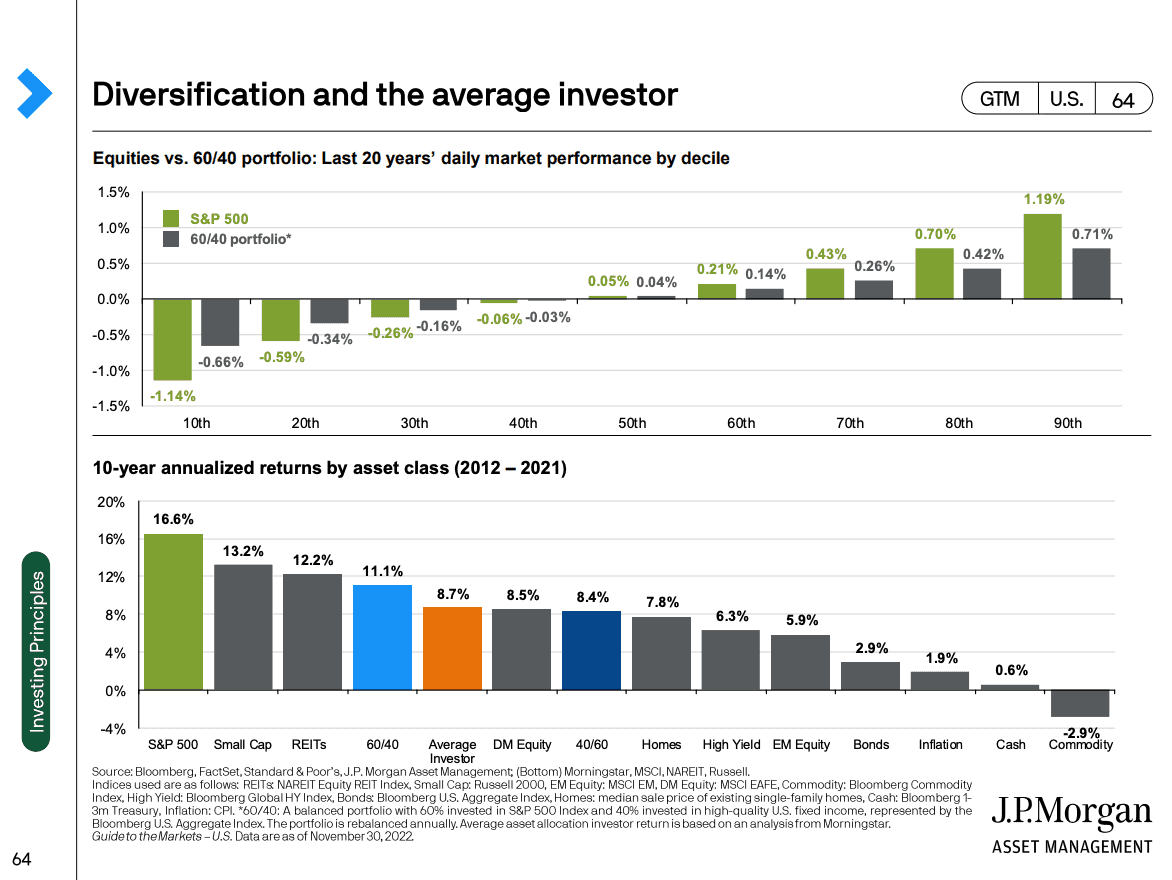

Average returns

JP Morgan used to publish a chart of an average investor’s 10-year returns. And they were a lot lower than you might think.

Source: JP Morgan Guide to the Markets Q4 2022

The average investor handily underperforms the S&P 500 over time. The biggest reason for this is psychological. Put simply, most investors just don’t have the patience to wait for opportunities. Instead, they chase quick returns.

The result is poorly-judged moves that ultimately lead to underperformance. But Berkshire Hathaway is (I hope) built differently. The average investor might want to see Berkshire make a big move. But given their returns, why would I want Abel to listen?

AI conundrum

The stock market theme of the last 12 months has been artificial intelligence (AI). And Berkshire Hathaway’s stayed well away.

There’s a good reason for this. In the 1994 shareholder letter, Buffett said:

“Just because Charlie and I can clearly see dramatic growth ahead for an industry does not mean we can judge what its profit margins and returns on capital will be as a host of competitors battle for supremacy.”

Even if AI’s here to stay, it’s not necessarily an opportunity. There’s still a question of who makes money from it. The big winner might be a company that doesn’t exist yet. Or, more worryingly, it might not be any companies at all.

Flight of fantasy

Buffett often cites the airline industry as a case study. It’s a technology that changed the world, but was a disaster for investors. This is because high fixed costs and value-focused customers forced down prices. And that’s true across the industry.

The big question is whether AI will be the same. And Berkshire’s view is that it isn’t in a position to rule this out. If they’re honest with themselves, I don’t think many investors are. But they’re willing to bet on the new technology anyway.

That’s the kind of strategy that leads to low returns. And I’m pleased to see that isn’t a road Berkshire’s going down.

Berkshire and AI

The rise of AI isn’t lost on Buffett’s firm. It increases the threat of a cybersecurity attack, which is a major risk.

Overall though, it’s largely ‘business as usual’ for Berkshire Hathaway. And I see that as a very good thing. Abel reiterated that Berkshire’s cash is an opportunity, but impatient investors will need to look elsewhere.

Source link