Image source: Getty Images

Ceres Power (LSE:CWR) is leading the FTSE 250 stock performance charts in 2026 and it’s not even close. Year to date, it’s up 176%!

That’s not too shabby considering we’re just four months into the year. And it easily beats the performance of some of the most popular stocks of the last year among UK investors, including Rolls-Royce (-5.2%), Nvidia (+13.3%), and BP (+32.3%).

Even more astonishing, however, is Ceres Power’s one-year performance, which now stands at 933% after the stock jumped 19% today (29 April).

What on earth has sent it stratospheric? And given that it’s still down 55% over a five-year period, might it be worth considering buying now? Let’s take a closer look.

What does it do?

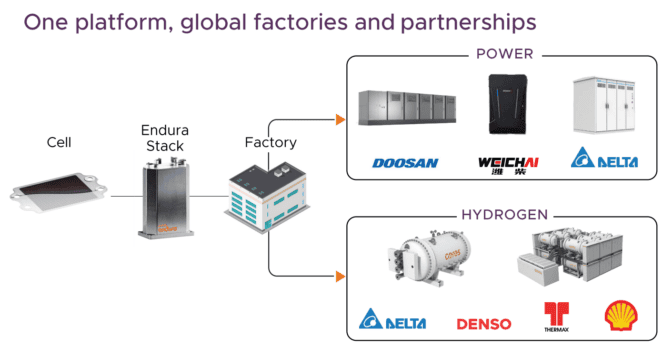

Ceres is a clean energy technology developer at the forefront of solid oxide fuel cell and hydrogen technologies. However, rather than building products, the company licences its IP to big industrial partners, including Doosan (South Korea), Weichai Power (China), and Delta Electronics (Taiwan).

In this sense then, Ceres is a bit like the Arm Holdings of the energy world. When successful, such asset-light licensing models can be wildly profitable and therefore very valuable. The company earned its first royalties last year.

When companies license our technology, they’re effectively bringing Ceres on board as their in-house R&D team. What they’re truly investing in is the ability to stay at the forefront of innovation, which is why we continuously invest in developing and safeguarding our intellectual property through innovation, backed by…the expertise of the world’s largest solid oxide team.

Ceres Power.

AI energy boom

As promising as this sounds, the stock’s almighty rise doesn’t appear to have anything to do with the company’s financials.

Last year, revenue was £32.6m, down from £51.9m the year before. Actual profits aren’t expected by City analysts in either 2026 or 2027.

No, the reason the stock is on fire is due to investor excitement around the data centre buildout to support artificial intelligence (AI).

The Philadelphia Semiconductor index, which is made up of the 30 largest US chip stocks, has rocketed 38% so far this month. It’s on course for its best month in 26 years, since just before the dotcom bubble burst.

Last month, Ceres announced a collaboration with Centrica to accelerate the deployment of solid oxide on‑site power solutions. It said this will enable “fast, scalable deployment of high‑efficiency, fuel‑flexible on‑site generation for data centres, AI compute hubs, advanced manufacturing, logistics and distribution centres“.

Fuel cells can be deployed much faster than traditional options, positioning Ceres as an emerging ‘picks and shovels’ player in the AI energy boom. And momentum-chasing investors continue to lap up these types of stocks.

Is Ceres still worth checking out?

In July, when the stock was trading at 143p, I said Ceres was worth considering for adventurous investors. I wrote that “the value of its IP may be very underappreciated right now“.

However, with the stock now near 600p, the valuation is a concern. We’re looking at a frothy price-to-sales ratio of 35.

Granted, on a forward-looking basis, this comes down to 19 because Ceres’ revenue is expected to almost double to £60m this year. But that’s still high for a loss-making firm.

Therefore, I think investors interested in the stock should tread carefully.

Source link