Image source: Getty Images

It doesn’t feel like the time to think about buying stocks. Collectively, shares are trading at some high multiples.

That, however, isn’t true across the board. And it’s a mistake to think that discounted prices means lower quality.

Robotics

Robotics is a big theme for investors at the moment. And one of the leaders in the field is Intuitive Surgical (NASDAQ:ISRG).

As the name suggests, the firm’s products are surgical robots. There are four reasons why this one’s on my radar:

- It’s a leading business in a growing industry.

- It’s protected by high switching costs.

- Its unit economics are extremely attractive.

- The stock is unusually cheap.

Together, I think these make a compelling case to at least look at the stock.

A growing industry

Whatever robots do in the future, they’re already having a big effect on surgical procedures. And this benefits both surgeons and patients.

Despite this, around 80% of procedures are still done manually. That means there’s still a long way to go in terms of market penetration.

Intuitive Surgical has a near-monopoly on robotic surgery. And this position is extremely difficult for competitors to disrupt.

With many surgeons trained on its system, hospitals have a strong incentive to prefer it. The same is true in reverse for surgeons looking for places to work.

This makes breaking Intuitive Surgical’s monopoly extremely tough. And in a growing industry, that’s an extremely attractive position.

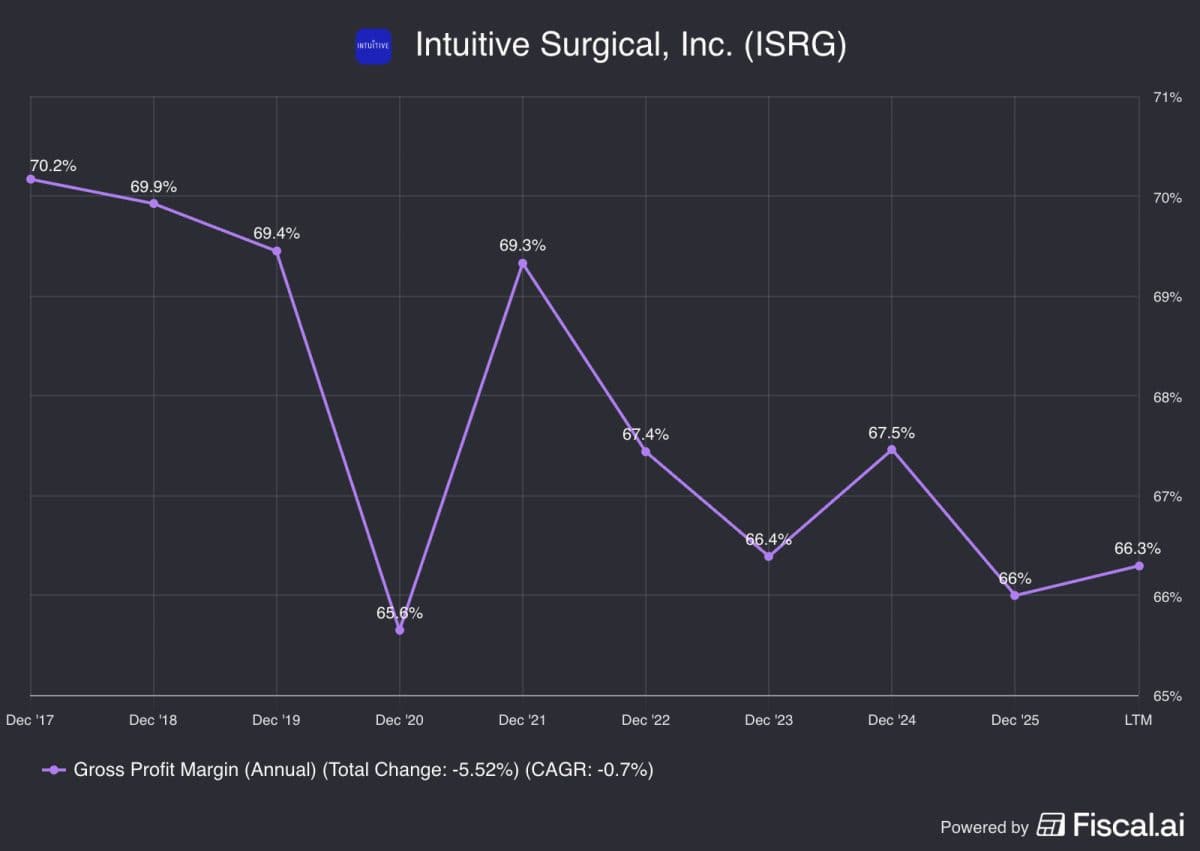

Unit economics

Intuitive Surgical consistently maintains gross margins above 66%. That’s extremely high, but it shouldn’t be a big surprise.

An installed base of equipment brings high-margin revenue. This includes ongoing servicing and replacement parts, but there’s something else.

Software stocks have been under pressure recently. But Intuitive Surgical’s simulation software is integrated into its hardware.

I think that’s an extremely attractive feature. And it’s one that’s very easy to miss in what looks like — and is — primarily a hardware business.

The company’s attractive margins are important for another reason. I think they give it a key advantage in tackling the biggest risk it currently faces.

The big risk

Intuitive Surgical’s equipment is expensive. That makes it vulnerable if – or when – budgets come under pressure or face uncertainty.

This has been an issue recently. The company, however, has been making moves to make it easier for customers to install new systems.

Rather than demanding millions of dollars up-front, it’s been offering a pay-as-you-go structure. That reduces the risk of under-utilisation for customers.

Instead, it transfers the risk to Intuitive Surgical. But the company’s size and scale mean it’s in a better position to handle that risk than its rivals.

As a result, it strengthens the firm’s competitive position even further. Offering more attractive terms helps increase the installed base of systems.

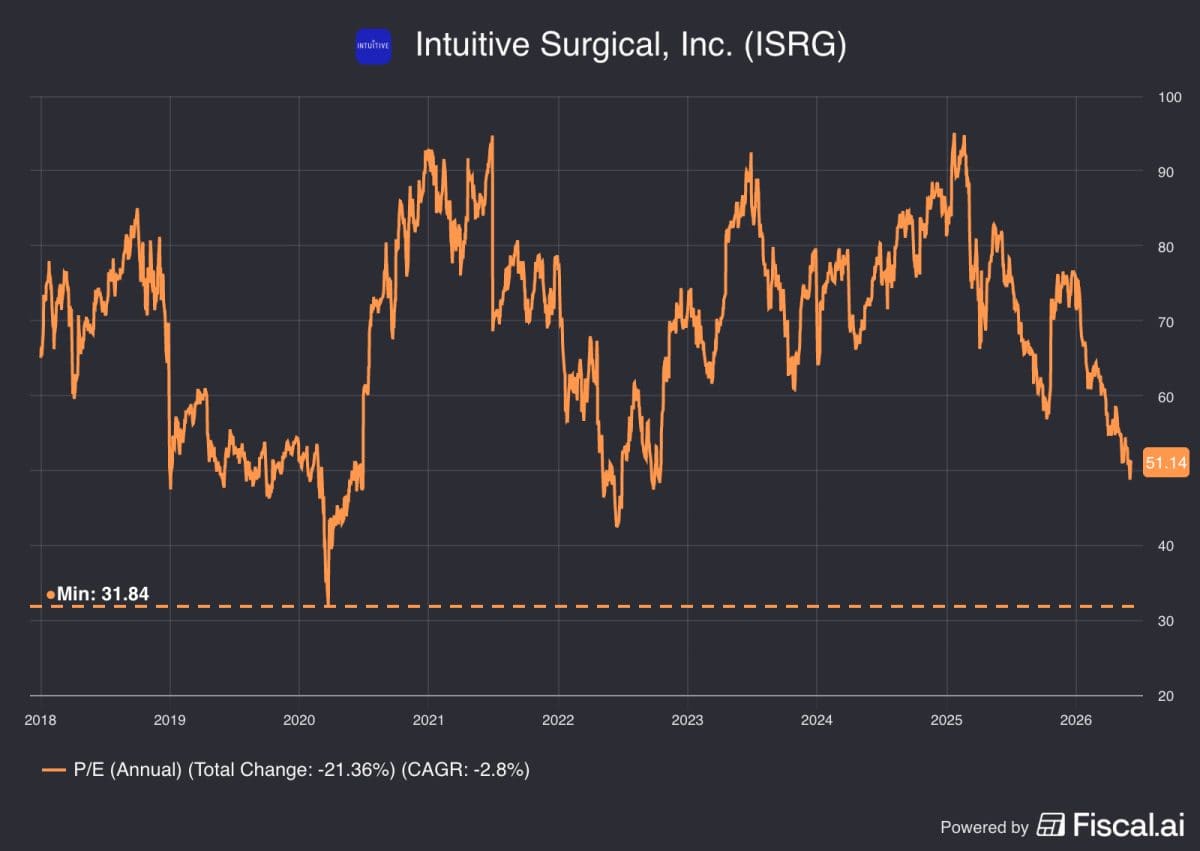

Valuation

I’ve had my eye on Intuitive Surgical for some time, but the stock hasn’t really looked cheap to me. Until now.

Based on next year’s earnings, shares are trading at a price-to-earnings (P/E) ratio of 35. The last time they were this cheap was in 2020.

That was during Covid-19 – when surgical procedures were getting cancelled. Are things really that bad right now?

I doubt it. And that’s why I think this might be an unusually good time to take a look at a high-quality stock.

Should you invest £5,000 in Intuitive Surgical right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Intuitive Surgical made the list?

Stephen Wright does not own shares in any of the companies mentioned.