Image source: Getty Images

The full new State Pension currently pays £12,547.60 a year. While that’s a valuable foundation, many retirees aspire to something more comfortable.

According to retirement industry estimates, a comfortable retirement can require annual income far above the State Pension alone. So what if an investor wanted to target three times the State Pension instead?

Crunching the numbers

How much would a Stocks and Shares ISA need to be worth to generate that level of income?

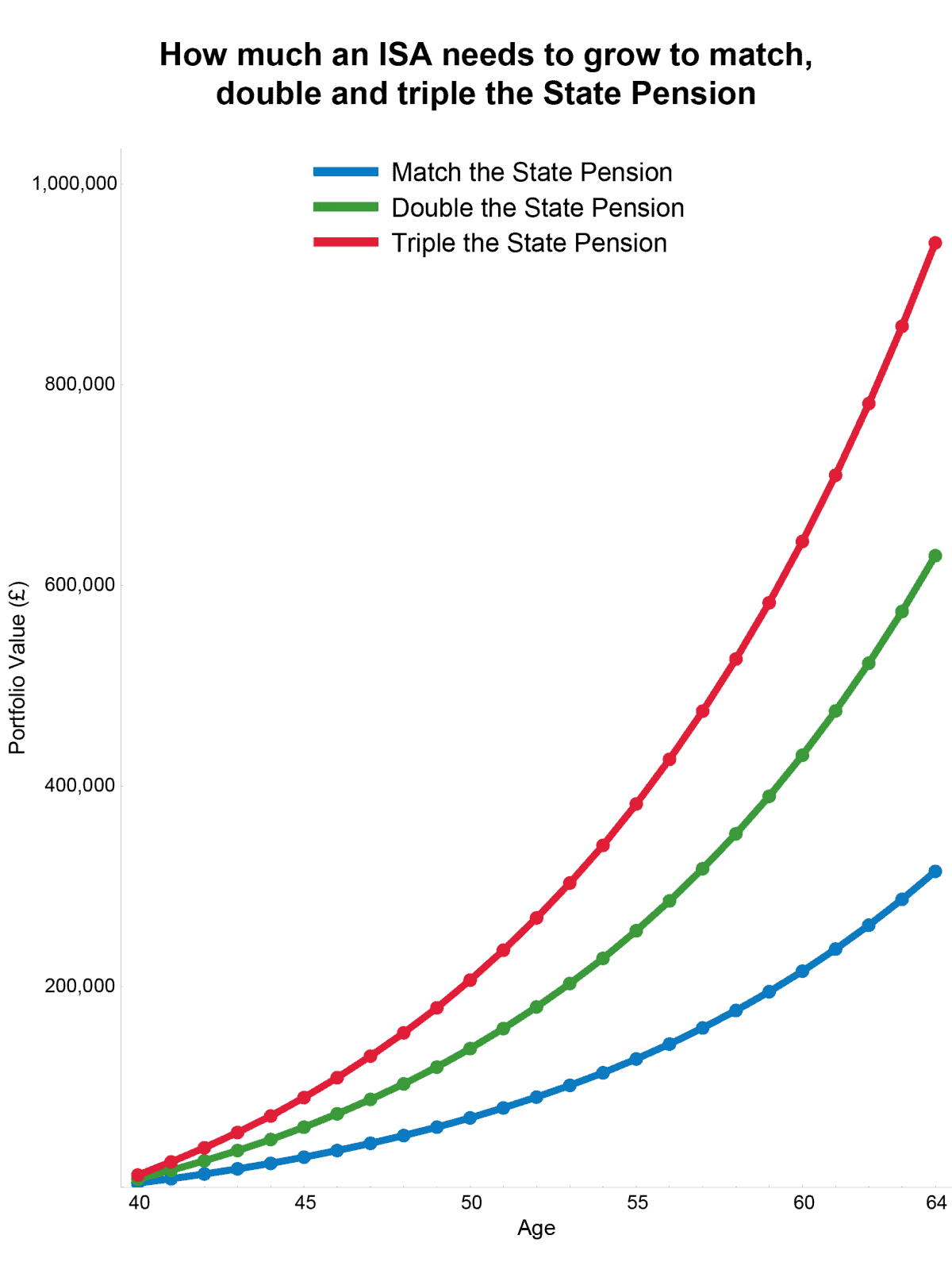

Using the widely respected 4% rule, the figures look like this:

- Matching the State Pension = £313,675

- Doubling the State Pension = £627,350

- Tripling the State Pension = £941,025

At first glance, those numbers are eye-watering. But the key point is that they are not designed to be built overnight.

Building it in real life

In practice, this is a long-term process driven by regular investing and compounding returns.

Assuming an 8% annual return over a 25-year horizon, the contribution path looks broadly like this:

- To match the State Pension, annual investing typically starts at around £4,000, gradually rising to £5,000 as savings capacity grow.

- To double the State Pension, contributions rise to roughly £8,000–£10,000 a year over the same period.

- To triple the State Pension, the requirement increases again to around £12,000–£15,000 a year, sustained over decades.

The exact figures will vary depending on market returns and timing. However, the relationship remains consistent: higher retirement income targets require a significantly higher and sustained level of investment.

Chart generated by author

Beyond high yield: compounding stability

Not every stock in an ISA needs to be a high-yield dividend payer. In fact, some of the most effective long-term holdings are those that quietly compound value over time.

That’s one reason I like RELX (LSE: REL). The group operates information and analytics platforms across legal, scientific, risk, and business data — areas where accuracy and trust matter more than speed alone.

The shares have been under pressure over the past year as investors worry about the impact of artificial intelligence. The concern is straightforward: if AI tools can generate summaries, draft analysis, and retrieve information instantly, could they weaken the role of traditional information providers?

At first glance, that argument is easy to understand. Large language models are improving rapidly, and they are already being embedded into professional workflows.

However, RELX is not simply a data provider. It sits inside regulated, precedent-driven industries where reliability, traceability, and accountability are essential. In these environments, raw AI output is not enough — it must be structured, verified, and integrated into professional workflows.

Rather than resisting this shift, the company is embedding AI into its own platforms, including tools like LexisNexis and its broader analytics suite. Management has also highlighted partnerships with leading AI developers to enhance, rather than replace, its existing services.

For long-term investors, the key point is consistency. RELX has delivered steady earnings growth, strong cash generation, and incremental innovation over time — all characteristics that support compounding within an ISA.

In the context of building a portfolio capable of bridging the gap between the State Pension and a more comfortable retirement, that kind of reliability matters just as much as high headline yields.

Should you invest £5,000 in RELX right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if RELX made the list?

Andrew Mackie owns shares in Relx.