Image source: Getty Images

I’ve occasionally compared Aston Martin (LSE:AML) shares to a James Bond motor after a high-speed chase — shattered and bullet-ridden, with plenty of red ink leaking from the carmaker’s financial statements.

However, like one of the fictional spy’s crumpled Aston Martins, this FTSE 250 stock soldiers on. In fact, it has jolted back into life in recent weeks, rising from 36p to 46p. This includes a 10% jump today (6 May).

So, had someone with a playful sense of humour invested £10,007 in Aston Martin on 1 April, they would now have about £13,550. But had they put the same amount in five years ago, the figure today would be less than £300!

Why’s the stock driving higher?

The stock’s recent move uphill can first be traced back to the company’s annual report, published on 25 March. At first glance, however, it’s quite difficult to see what was so positive.

Revenue slumped 21% to £1.26bn, while the pre-tax loss widened from £289m to £364m. The carmaker was hit by a hurricane of challenges, ranging from tariffs and weak sales in the US and China to production delays with its high-priced special models.

However, in the fourth quarter, Aston Martin delivered 152 of its $1m Valhalla plug-in hybrid supercars. These high-margin beasts helped raise the average selling price (ASP) to £232k, up from £178k in the previous quarter, and drove quarterly cash flow into positive territory.

The company has other high-performance vehicles out, including the Vantage S and DBX S. The latter was voted super SUV of the year in 2025 by Top Gear Magazine.

As an aside, I saw a new Aston Martin Vanquish Volante convertible recently. Parked up with its beautiful sage green paintwork glistening in the sun, the car had a small admiring crowd around it, with some taking snaps.

God only knows what reaction the Valhalla gets!

Improving financials

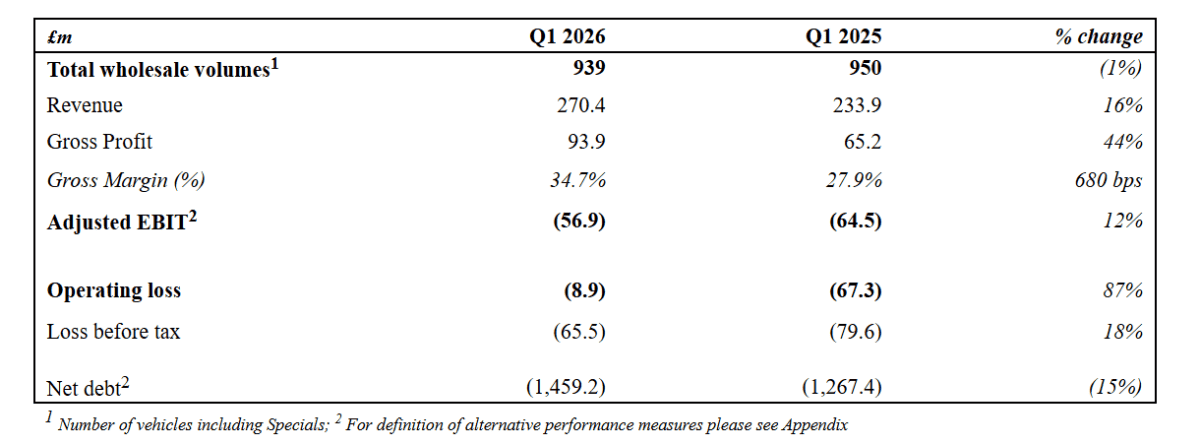

The momentum continued into the first quarter of 2026, as the firm delivered another 102 Valhallas. This saw the gross margin improve 680 basis points to 35%, and the ASP rise 17% year on year.

The operating loss reduced from £67.3m to just £8.9m. And management sees the annual adjusted operating loss narrowing to £92m from £189m last year.

Finally, Chair Lawrence Stroll’s consortium pumped in another £50m, bringing liquidity to around £230m.

Am I tempted?

As a big fan of the brand and cars (confession: I was one of the Vanquish Volante admirers), I’m very tempted to scoop up some shares around 46p. I don’t like seeing Aston Martin in semi-obscurity in the FTSE 250.

However, that’s my heart speaking. My head sees the bottom line in the table above. Net debt of £1.46bn was up from £1.27bn the year before. And financing costs were the main reason why the adjusted pre-tax loss widened to £114m, despite the operational progress.

Another thing that worries me is the ongoing situation in the Middle East, which is packed with wealthy Gulf buyers who might not be in the mood for new sportscars this year. The luxury market in China remains very challenging.

If Aston Martin can keep making progress, adventurous investors might make a fortune buying at 46p today. But I’m still not convinced enough to invest myself.

Source link