Image source: Getty Images

Stocks and Shares ISA investors have just days left to use up their £20,000 allowance before the April 5 deadline. Once it passes, any unused allowance is lost for the year.

That’s what makes this moment so important.

Because while markets may feel uncertain right now, time in the market — not timing the market — is what really builds wealth. And the earlier money is invested, the harder it can work in the background.

It’s easy to underestimate just how powerful that can be. Small, consistent investments — given enough time — can snowball into something far larger, driven not just by returns, but by returns on those returns. In other words, compounding.

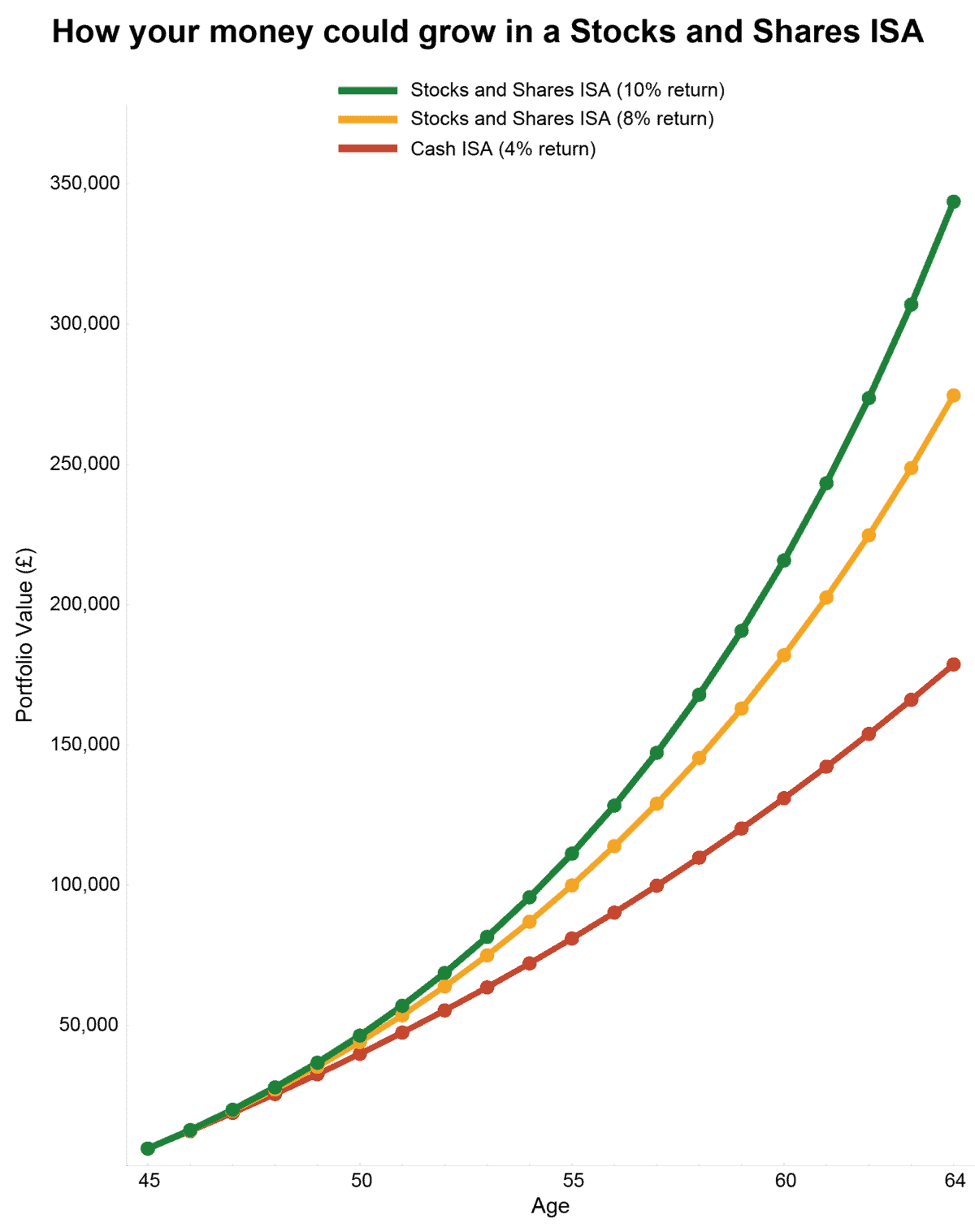

That might all sound theoretical, so let’s put it in perspective. The chart below shows what compounding £500 a month could actually deliver over 20 years.

Chart created by author

The £170,000 difference you could be missing

Investing £500 a month could grow to around £180k at 4%, £275k at 8%, or as much as £350k at 10%. That difference isn’t pocket money — it’s the real impact of putting money to work sooner rather than later.

A Stocks and Shares ISA give investors the chance to aim for those higher long-term returns — while keeping every penny of the gains and income tax-free. With the April 5 deadline fast approaching, the real risk isn’t short-term market swings. It’s missing the chance to get that money working at all.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

High-yield stock

Headline-grabbing yields don’t come much higher than Legal & General (LSE: LGEN). The forward yield is 9.6% — exceptionally rare for a FTSE 100 stock — giving investors a chance to lock in meaningful income while compounding tax-free.

FY25 results showed solid progress on strategic targets. Core operating earnings per share grew 9%, at the top of its three-year target of 6%–9% compound annual growth. The Solvency II coverage ratio, a key measure of balance sheet strength, stood at 203%.

It also launched a £1.2bn share buyback programme — the largest in its history — funded overwhelmingly by the sale of its US protection business.

Balancing risk with reward

The asset manager isn’t without challenges. RBC Capital Markets recently turned bearish, highlighting rising competition in the lucrative pension risk transfer market and noting that higher inflows in asset management aren’t yet translating into profit growth.

But look 10 years out, and the picture is far brighter. The UK retirement market is set to triple, driven by the continued rise of defined contribution schemes.

Demand for annuities should remain strong in a structurally higher interest rate environment, while the company’s scale and market-leading franchises position it to benefit from these long-term trends.

For my ISA, Legal & General remains a high-yield anchor — a stock I can add to steadily, collecting income today while backing structural growth over the long term. The 9.6% yield is not something to ‘lock in’ ahead of any deadline, but starting earlier rather than later simply gives more time for dividends to be reinvested and compound tax-free within the ISA wrapper.

Opportunities like this, particularly in volatile markets, are not always available at attractive valuations.