Image source: Getty Images

The best time to buy shares is when investors are looking for opportunities elsewhere. And even the best businesses go through times when they’re out of fashion with the stock market.

The incredible growth Nvidia (NASDAQ:NVDA) has achieved recently isn’t really showing signs of slowing. But with the stock down since the start of the year, is it time to take a look?

Size

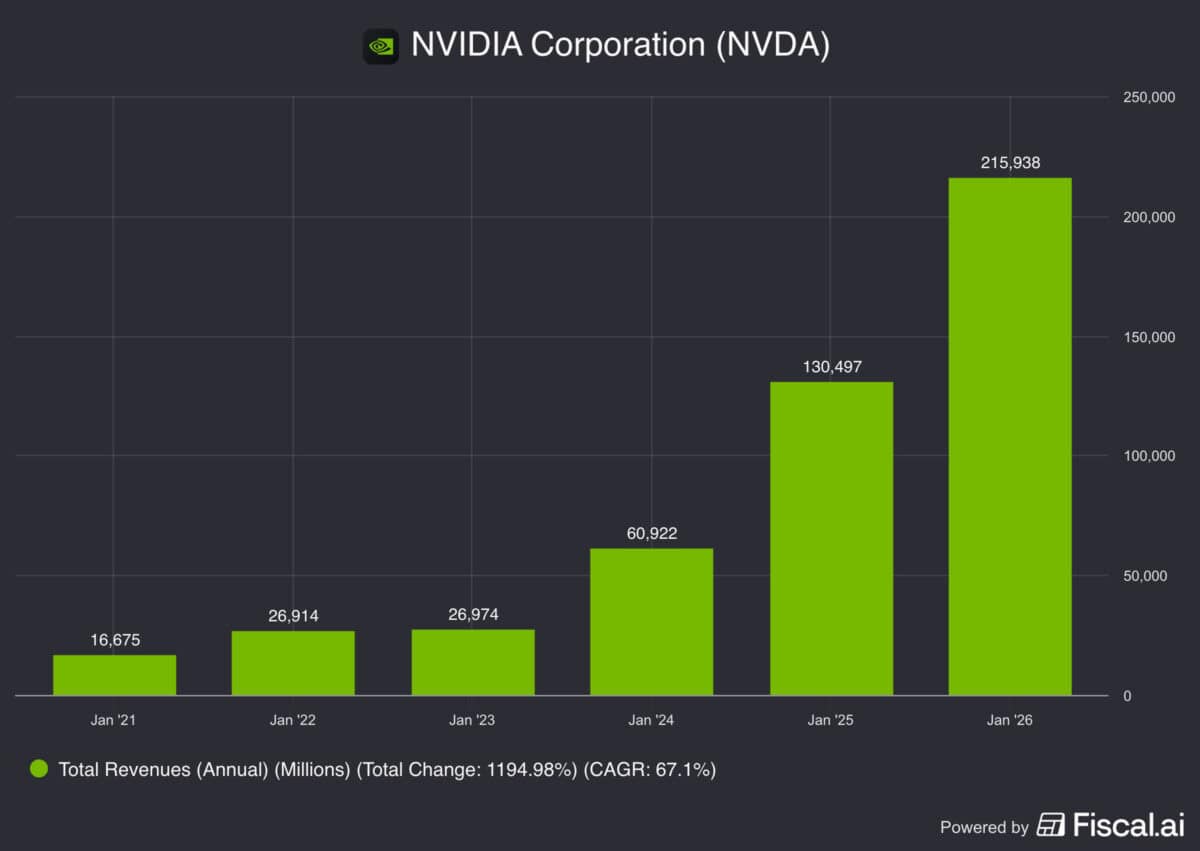

Nvidia’s growth since 2021 has been the stuff investors dream of. Revenues have gone from $16.6bn to $215.9bn in the last five years, at an average annual increase of 67%.

Some investors, though, are starting to get concerned about this. They worry that it gets a lot harder for the company to maintain a high growth rate as its sales figures go from big to huge.

There’s some truth to this, but I don’t think there’s a real cause for alarm. Nvidia’s revenues are still only about 50% of what Alphabet and Apple make in annual sales, even at $215.9bn.

That means the company isn’t exactly in uncharted territory, or in fact anywhere near it. So I think there’s still a way to go until Nvidia’s size gets in the way of its growth prospects.

Valuation

Nvidia isn’t in uncharted territory in terms of sales figures, but it is when it comes to market value. At $4.4trn, it takes a lot to make the stock go higher from this point.

By itself that’s not a major concern. There’s no fixed limit on how high a stock can go and certainly no rule that says whatever goes up must come down.

Furthermore, the share price stagnating as the company keeps growing means the gap between sales and market value has been closing. That does help limit the risk for investors.

Ultimately, though, the future of the stock is going to depend on how the underlying business performs. And a big part of this is the demand outlook.

Supply and demand

Investment in AI data centres has been huge, but it isn’t showing any signs of slowing down. Earlier this week, Oracle reported a backlog of $553bn – a 325% increase from last year.

That can only be good for Nvidia and the stock is trading at a forward price-to-earnings (P/E) ratio of 23. That level implies expectations of strong, but not necessarily explosive, growth.

The demand side of the equation looks strong, but investors should also keep an eye on supply. Increasing competition – including from Nidia’s customers – is a real threat to keep an eye on.

Regular product upgrades have been a key part of Nvidia’s growth story and this is likely to remain the case going forward. So new alternatives are probably the biggest threat right now.

Time to buy?

I don’t think there’s any question that Nvidia’s shares are better value than they were at the start of the year. But are they better value than other stocks available to buy right now?

I’m less convinced about this. It’s not just a matter of multiples – Nvidia’s don’t look too bad to me – but I think there are more attractive opportunities elsewhere at the moment.