Saudi Arabia is set to cut oil production amid fears the Middle East crisis will leave Brits facing the highest ever pump prices.

The Kingdom – the biggest supplier in the region – is said to be curbing output at two major oilfields, although the extent of the reductions are not clear.

The news emerged as experts warn that petrol could hit £2 a litre for the first time, amid a staggering spike in global oil costs.

Keir Starmer is desperately trying to calm fears of another 2022-style cost of living squeeze, hinting at another bailout despite the fragile state of the government’s finances.

On a visit to a community centre in London this morning, Sir Keir insisted the economy is more ‘resilient’ than when Russia’s full-scale invasion of Ukraine cause havoc four years ago.

But he conceded that the longer the war goes on ‘the more likely the impact on our economy’, urging ‘de-escalation’.

Sir Keir is also scrambling to limit damage to the Special Relationship from his refusal to back Donald Trump’s decision to launch the war on Iran.

The president has dismissed the soaring oil and gas prices saying they are a ‘small price to pay’ for taming Tehran.

The price of a barrel of oil has rocketed over $100 for the first time in years, with supplies threatened by attacks on infrastructure of major producers in the region.

Iran has also managed to effectively shut the Strait of Hormuz, through which around a fifth of the world’s oil travels.

Analysts say there is a real risk the oil price will reach $150 a barrel, with estimates that would mean £2 a litre petrol for British drivers. The previous record was 191.4p in 2022, and they are currently running around 140p.

An emergency meeting of the G7 has been called for today, where Rachel Reeves will join other ministers discussing options including the release of oil reserves.

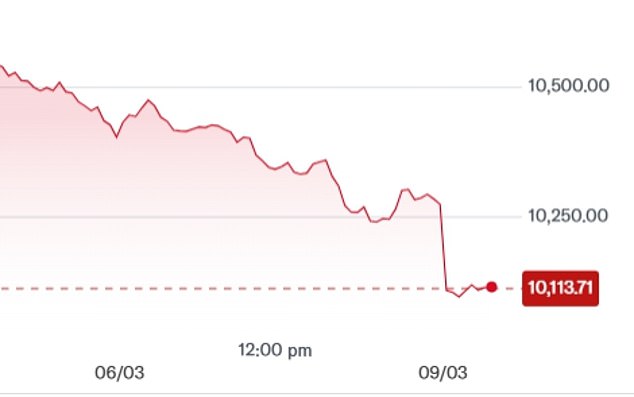

The FTSE 100 dropped more than 100 points on opening this morning, having lost well over a month of gains since the crisis erupted nine days ago.

In other dramatic developments today:

- Ministers are trying to quell concerns about the UK’s low gas storage, which could mean consumers are more exposed to rising prices;

- Sir Keir has hinted that his call with Mr Trump yesterday was icy, insisting he had to act in the UK’s ‘best interests’. It was the first time the leaders have spoken in more than a week, following a series of insults aimed at him by the president;

- Hopes the Bank of England could cut interest rates this month have been effectively wiped out by the prospect of a new inflation spike;

- Fears are growing that the Chancellor will need more tax increases to balance the books, as debt interest cost increase and the economy comes under pressure;

- The Tories are trying to force a vote on the government’s plans for a staged 5p increase in fuel duty from September;

- Emmanuel Macron is expected to visit Cyprus amid Britain’s embarrassing inability to protect the RAF Akrotiri base from Iranian reprisals;

- HMS Dragon is still at Portsmouth and is unlikely to arrive in Cyprus to protect Akrotiri for another week;

The FTSE 100 fell sharply in early trading this morning

Keir Starmer is desperately trying to calm fears of another 2022-style cost of living squeeze, hinting at another bailout despite the fragile state of the government’s finances

A thick cloud of black smoke hangs over Tehran after the Shahran oil depot was hit in a fresh round of US-Israeli strikes

Explosions erupt following strikes in Tehran over the weekend

Iran’s Revolutionary Guard has threatened to ‘set ablaze’ any Western tanker that attempts to navigate the strait.

Hundreds of ships laden with oil, as well as liquefied natural gas, have amassed either end of it.

Iraq and Kuwait have begun cutting output, with the UAE and Saudi Arabia expected to follow suit as they run out of oil storage.

The price of a barrel of Brent crude was nearly 30 per cent higher in Asian markets at some points overnight, as traders concluded that the crisis will drag on.

It took just a minute for the price to rise by 10 percent, and 15 minutes for another 10 percent, seeing it surge beyond the $100 mark for the first time since the early days of Russia’s invasion of Ukraine in 2022.

But a defiant Mr Trump wrote on his Truth Social site: ‘Short term oil prices, which will drop rapidly when the destruction of the Iran nuclear threat is over, is a very small price to pay U.S.A., and World, Safety and Peace.

‘ONLY FOOLS WOULD THINK DIFFERENTLY!’

On his visit this morning, Sir Keir struck a different tone, saying he was looking at ways to ‘reduce the likely impact’.

‘The job of government is obviously to get ahead, to look around the corner, to work with others, and the Chancellor speaks to the governor of the Bank of England on a daily basis, with looking cross-departmental within government, assessing the risks, monitoring and talking to our international partners as well about what more we can do together to reduce the likely impact on people here and businesses here, of course,’ the premier said.

‘But it is important to acknowledge that that work is needed, because people will sense, you will sense I think, that the longer this goes on, the more likely the potential for an impact on our economy, impact into the lives and households of everybody and every business.

‘And our job is to get ahead of that, to look around the corner, assess the risk, monitor the risks, and work with others in relation to that.’

He added: ‘I think it is important just to remind ourselves that last time a conflict began to develop, which was 2022 in relation to Ukraine, the economy wasn’t in a stable place, and inflation was 5 per cent and rising.

‘We’ve done a lot of work in the last 18 months to put some resilience in and make sure that we’ve got some headroom, which is basically some insurance within the economy, but also inflation is 3 per cent and going down, so in that sense, there’s more resilience.’

Asked whether Mr Trump was risking a third World War, Sir Keir said: ‘We do need to find a way to de-escalate the situation and that’s what a lot of our discussions are about – how do we find a way to de-escalate this situation and make sure it doesn’t escalate even further than it already has.’

Interest rates on 10-year gilts – one of the main ways the government borrows money – were up another 0.14 percentage points this morning. They are up around half a percentage point since the war erupted.

Oil reserves are co-ordinated by the International Energy Agency (IEA), with 32 members of the group holding stocks as part of a collective emergency system designed to mitigate oil price crises.

Three G7 countries, including the US, have so far indicated their support for a possible joint release, according to the FT.

Escalations over the weekend, alongside scenes of destruction of energy infrastructure both in Iran and across the Gulf, contributed to a sharp shift in mood on markets.

Donald Trump has dismissed the soaring oil and gas prices saying they are a ‘small price to pay’ for taming Tehran

Natural gas costs have soared since the US-Israeli strikes began, raising alarm about the impact on energy bills

Economist Julian Jessop

The OBR has warned that even before the crisis the tax burden was on track to reach never-before seen mark of 38.5 per cent of GDP in 2030-31

A slump in the stock market has deepened, after the S&P 500 and Stoxx Europe 600 sliding 1.6 percent and 2.1 percent respectively.

The FTSE 100 was 181 points – 1.8 per cent – lower at 10103.71 within the first 10 minutes of trading. The FTSE 250 Index was even harder hit, falling 2.3 per cent.

Fears emerged yesterday that Britain was also in trouble over its stocks of natural gas.

Figures suggested that, in a worst-case scenario, the country could have just two days’ worth of demand stored up.

Reserves dwindled from 18,000 GWh last year to the current 6,700 GWh, enough for just 1.5 days of demand, according to new data published by National Gas. There is a similar quantity stored as liquefied natural gas (LNG).

Touring broadcast studios for the government this morning, Communities Secretary Steve Reed insisted stores were at normal levels for the time of year.

He told ITV’s Good Morning Britain: ‘Of course, the UK can’t control things that happen, crises that happen across the planet, that have an impact on us here at home.

‘What we can control are our own circumstances.’

He said in last week’s Spring Statement Ms Reeves was able to ‘point to those benefits of a more stable economy thanks to her stewardship of the economy, that puts us in a better position to weather whatever storms might come our way’.

He added: ‘Now, when it comes to the cost of oil, and we’ve seen what’s happened overnight, we’re still only just over a week into this conflict, we don’t know how long it will go on, we don’t know what the long-term impact will be on energy prices.

‘But, as I say, the fact that we have a more stable economy means we’re in a better position to weather those storms, and we will, of course, keep a very close eye as we monitor the situation.’

The Chancellor has already imposed an astonishing £75billion a year of extra tax on Britons since Labour came to power. The Spring Statement last week revealed that the burden is heading to a new record high.

Much of that has gone on spiralling welfare costs, with Labour MPs forcing the government to abandon efforts to curb spending and scrap the two-child benefits cap.

Ms Reeves boasted about the government’s finances improving last week, but the Treasury’s OBR watchdog had not factored in any of the impact from the Iran turmoil.

And it made clear Ms Reeves was balancing the books largely on the basis of a tax windfall from surging stock markets.

The OBR cautioned that a 35 per cent correction would add £26billion to borrowing, effectively wiping out the Chancellor’s ‘headroom’ for hitting her main fiscal targets. The FTSE 100 has already lost around 8 per cent in the past week.

Iran named Mojtaba Khamenei to succeed his father Ali Khamenei as Supreme Leader yesterday.

That sent a signal that regime hardliners are still firmly in control of the country, drawing fresh fury from Mr Trump.

Announcing the news, Iran’s foreign ministry said: ‘The selection of the new leader of the Islamic revolution at a time of grave challenge will reinforce national unity and safeguard the country’s independence, sovereignty and territorial integrity.’

US Defense Secretary Pete Hegseth ramped up the rhetoric again last night, guaranteeing Iran will ‘surrender’ and Mr Trump will set the terms of their defeat.

Mr Hegseth sat down for an exclusive interview with CBS News’ ’60 Minutes,’ where he was asked what the president meant by his demand for an ‘unconditional surrender.’

‘It means we’re fighting to win. It means we set the terms,’ the Defense Secretary replied.

Oil tankers anchored outside the Strait of Hormuz