When my daughter was born, one of the first things I did was open a SIPP (Self-Invested Personal Pension) in her name. It might sound premature — after all, retirement’s at least 55 years away for a newborn.

But that’s precisely the reason to do it. Time is the single most powerful ingredient in wealth creation, and a SIPP opened at birth has more of it than almost any other investment vehicle.

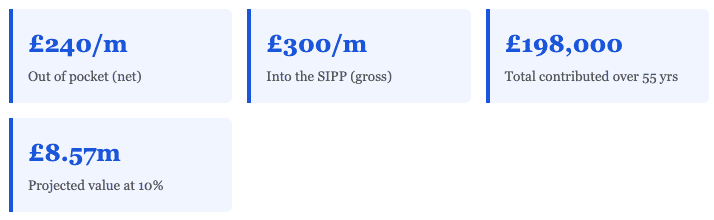

Here’s the beautifully simple maths. When I contribute just £240 a month into a Junior SIPP — that’s the equivalent of around £55 a week — the government automatically tops it up with 20% tax relief, bringing the gross contribution to £300 a month, or £3,600 a year. That’s the current maximum annual allowance for a non-earner.

At a 10% average annual growth rate, compounded monthly over 55 years, that £300 a month snowballs into approximately £8.6m. The total amount actually contributed? Just £198,000.

The rest — which is over £8.3m — is generated purely by compound growth. It’s pretty much the closest thing to financial magic that exists.

Image source: Getty Images

It’s very achievable

Now, 10% might sound ambitious, but it’s broadly in line with the long-run average return of the stock market. The S&P 500, for instance, has returned around 10%-11% annually over the past century. Of course, past performance doesn’t guarantee future results, and there will be stomach-churning drops along the way. But over a 55-year horizon, history suggests the odds are firmly in your favour.

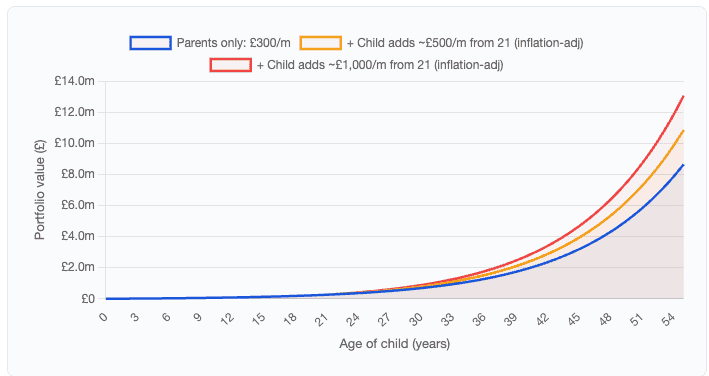

And here’s where it gets really exciting. Those figures assume the parents or grandparents shoulder the full cost for 55 years. In reality, at some point the child grows up, gets a job, and can start contributing themselves. If they begin adding to the pot from age 21, the numbers become truly staggering.

| Scenario (10% growth) | Value at 55 | Total contributed |

|---|---|---|

| Parents only: £300/m for 55 years | £8,574,424 | £198,000 |

| Child adds £500/m (inflation-adj) from 21 | £14,853,736 | £402,000 |

| Child adds £1,000/m (inflation-adj) from 21 | £21,133,048 | £606,000 |

Where to invest?

This is the million-dollar question. However, here’s some things to consider. The portfolio will start small, so it may be best to make fewer trades (limit transaction costs). That might mean taking a single stake in a fund or trust that offers instant diversification across companies.

One trust that continues to attract my attention is Scottish Mortgage Investment Trust (LSE:SMT). The investment trust has a great track record of picking the next big winners, and will hopefully be able to navigate some of the upcoming AI upheaval. Scottish Mortgage has positions in the likes of TSMC, Mercadolibre, ASML, and Nvidia. These are technology leaders, and three out of the four have performed very well over the past year.

But the largest holding by some margin in SpaceX. And I like that. If I had to take a guess at what I think will be the biggest company in the world in a decade from now, I’d say SpaceX. I could be very wrong, but I think there’s a very compelling argument to believe SpaceX will dominate the space economy.

Risks? Well, Scottish Mortgage uses gearing — borrowing to invest. This can heighten gains when stocks go up, but magnify losses when investments go down.

Nonetheless, this could be an excellent long-term vehicle for a passive investor. I think it’s worth considering.