For the first time in ages, many high-quality tech stocks are looking cheap. In particular, I’m thinking about ones that have been dumped due to fears about potential artificial intelligence (AI) disruption coming down the pike.

Admittedly, such concerns are warranted in some cases as the technology’s very disruptive and advancing rapidly.

That said, I think some babies are being chucked out with the murky bathwater. And over time, these shares could deliver market-beating returns from their currently depressed valuations.

One S&P 500 company I have in mind is trading very cheaply despite still growing at a decent clip. Moreover, it’s turned into a voracious cannibal!

What’s a ‘cannibal’ stock?

A cannibal stock has nothing to do with horror movies. It’s simply a company that’s consistently ‘eating’ itself by aggressively buying back its own shares on the open market.

So instead of spending the cash on acquisitions, more R&D, or special dividends, these cannibals use their free cash flow to drastically reduce the total share count.

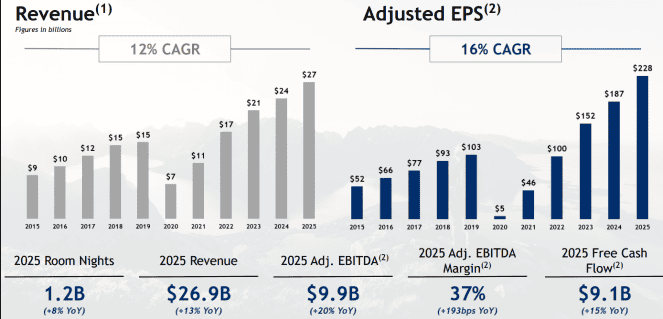

The example I have in mind is Booking Holdings (NASDAQ:BKNG), the world’s largest travel booking platform. Between 2022 and the end of 2025, the company reduced its share count by 22%.

Now, what I like here is that this was after accounting for dilution. That is, the shares that are handed out to executives and other employees. In Q1, Booking bought back another $3.6bn worth of shares, with a total remaining authorisation of $18.2bn. So the feast is set to go on.

The benefit to shareholders here is twofold. First, it increases their ownership of the underlying business without doing a thing. Second, earnings per share automatically shoots up because there are fewer shares.

Normally, buybacks would be a positive catalyst for the share price. Yet Booking stock’s down 22% over the past 12 months. Why?

What’s the catch?

The concern some investors have is that people could use AI platforms/agents to book accommodation in future. This could see Booking’s growth slow and its take rate (averaging about 15% worldwide) come under pressure.

Such disintermediation — or cutting out the middleman — is a key risk. However, as things stand, I think it’s overblown. You see, almost 90% of Booking’s accommodation business comes from independent hotels or small alternative accommodations, which aren’t sophisticated. The company handles payments in dozens of currencies, offers fraud prevention, and trusted customer service (easy cancellations, refunds, etc).

Will consumers authorise an AI agent to book on a hotel website in a foreign country, with no central platform (like Booking) providing 24/7 post-booking support and guarantees? Perhaps, but I doubt most will anytime soon.

What if it books Birmingham, Alabama instead of Birmingham, England? If every AI assistant needs a supporting layer underneath, the companies that already provide that infrastructure will remain valuable.

Meanwhile, customer habits are slow to change. Speaking personally, I like to check photos of the bathroom and balcony myself, and I value Booking’s reward programme.

What about valuation?

The stock’s trading at just 17 times forward earnings. For such a profitable firm buying back a ton of shares, I think this is too cheap. Wall Street thinks so too, with the 12-month price target currently 24% higher.

Stitching all this together, I reckon Booking is undervalued and worth checking out.

Should you invest £5,000 in Booking Holdings right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Booking Holdings made the list?

Ben McPoland has no position in any of the companies mentioned.