Image source: Getty Images

UK shares have spent the best part of the last 20 years asleep. But a couple of charts buried in JP Morgan‘s latest Guide to the Markets suggest the mood might be about to shift.

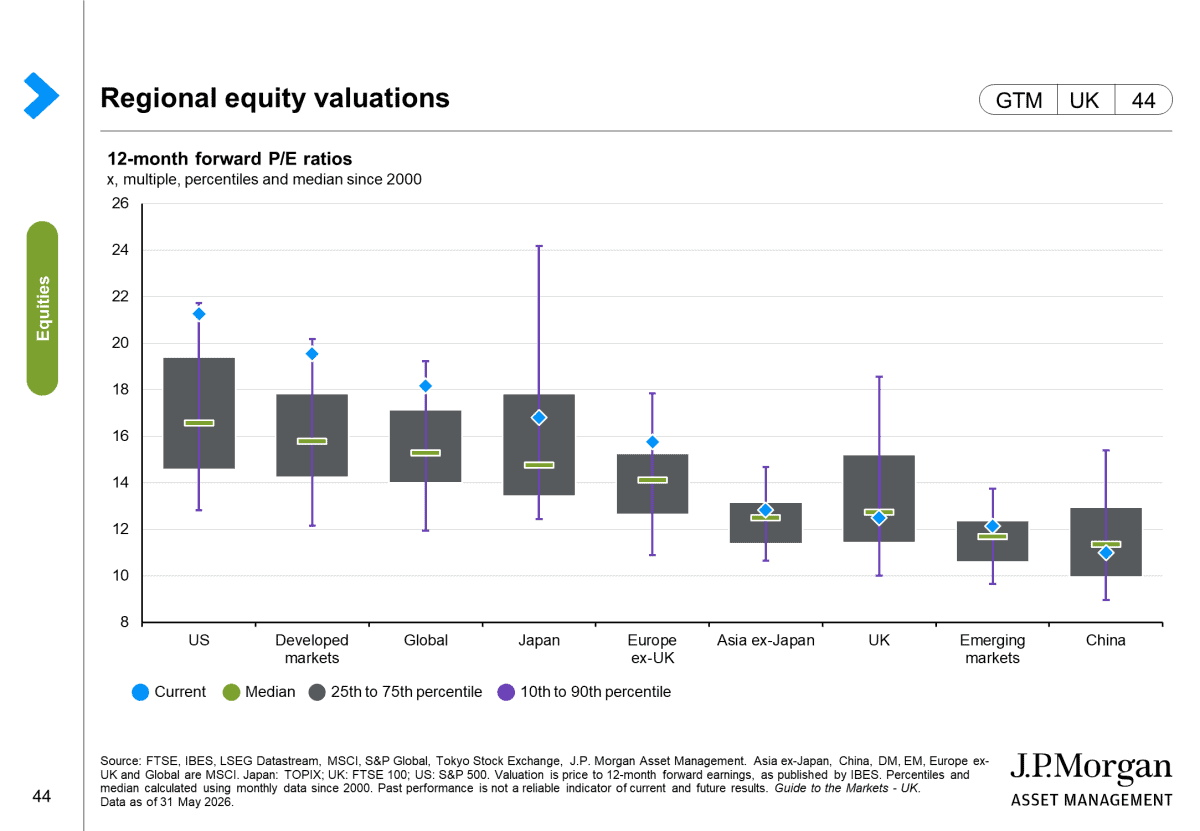

UK stocks are cheap right now

On a 12-month forward price-to-earnings basis, the FTSE 100 trades at around 12.6 times. Only China sits lower among the major markets JP Morgan tracks.

The US, by contrast, is on 21.3 times. That’s not a rounding error, it’s a 70% premium for owning the same world, just with better tech stocks and a stronger sense of its own destiny.

Source: JP Morgan Guide to the Markets

A discount that size means either Britain is heading for the economic equivalent of a rain-soaked Wimbledon final, or the market has simply stopped paying attention. Or both.

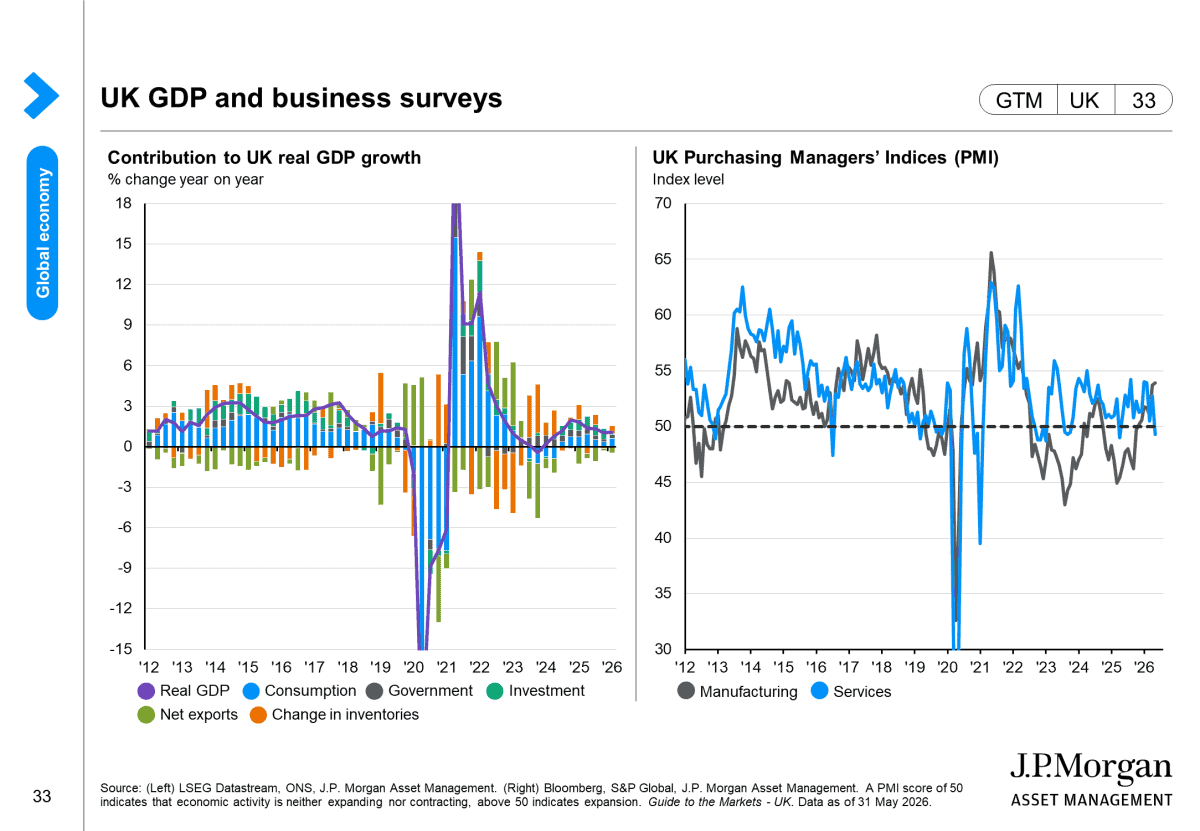

Reading the manufacturing tea leaves

The other chart worth paying attention to is the UK’s Purchasing Managers’ Indices. It’s a key leading indicator of economic activity – and it looks interesting right now.

While Services has been losing momentum, Manufacturing has been doing the opposite. That’s a change from normal service.

Source: JP Morgan Guide to the Markets

For most of the last 15 years, Services has been leading the way while Manufacturing has faltered. But the latest shift creates an interesting setup for value investors.

A factory sector that’s stopped shrinking, underneath a market this cheap, is worth a look. Don’t call it a comeback, but it’s the kind of thing diligent investors tend to notice.

Where to look?

What does the UK manufacture these days? One answer is bricks, but the housing market isn’t encouraging.

Another answer is defence stuff. With the likes of BAE Systems, Babcock, and Rolls-Royce, weapon-grade weapons are still a strong suit for British manufacturing.

As an additional boost, Keir Starmer just confirmed an extra £15bn for defence over the next four years. Exactly where that comes from might be Andy Burnham’s problem.

For a lot of investors, this kind of news is the cue to buy some of the names above. But I’ve been looking at a different stock.

Under the radar

Cohort (LSE:CHRT) is a defence tech company. It makes things like communication, sonar, and surveillance systems that go submarines and other vehicles.

The firm recently posted full-year revenue up 12% to £303m, with a record order book of £620m. That’s about 80% of next year’s expected revenue already locked in.

Here’s what I like about the company:

- Order intake of £313m outpaced revenue again, the third year running

- Communications and Intelligence margin jumped to roughly 20%, from 16.8%

- A €42.3m Portuguese Navy contract shows export demand isn’t just a UK story

Starmer’s package should provide a further boost. But it’s worth noting that a change of leader means the funding gap not being filled is a real possibility.

Even so, Cohort’s order book was built well before this week’s announcement. That means it’s a welcome boost, rather than a crucial requirement.

Buy in July?

Cohort shares are up 42% since the start of the year. But there’s a lot going the company’s way at the moment.

I don’t think investors should be too quick to conclude that the time to buy this one has passed. I can still see a lot worth paying attention to.

Should you invest £5,000 in Cohort Plc right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Cohort Plc made the list?

Stephen Wright does not own shares in any of the companies mentioned.