Image source: Getty Images

Tesco‘s (LSE:TSCO) share price has been slipping ahead of today’s Q1 trading statement. It’s dropped another 2% after the statement’s release, suggesting investors weren’t expecting much — and still came away disappointed.

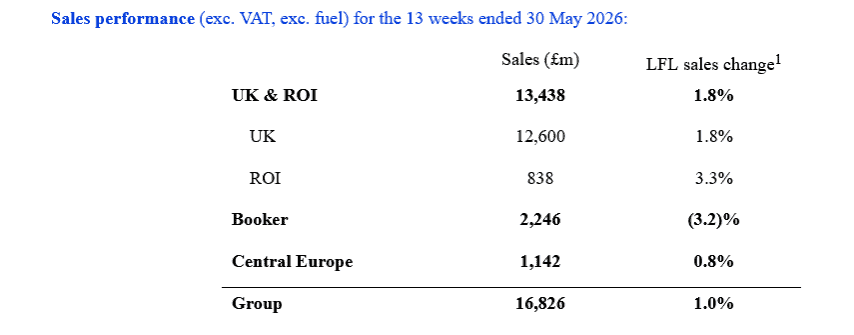

So, what’s happened? Tesco’s like-for-like takings in the three months to May were up just 1% year on year, excluding fuel. City analysts had expected them to rise 1.4%.

The thing is, I think things could get much tougher for the FTSE 100 company and its share price. Want to know why?

Disappointing Q1

Food retail is one of the most stable industries out there. And Tesco is the sector’s biggest player, with millions of loyal customers and incredible scale that keeps costs down. Analysts at RBC Capital have described the firm as the

Best-in-class player in the UK Food Retail space, with a strong business model and an experienced management team.

It’s quite possible you shop at Tesco in store or online yourself. I nipped into my local just this morning to pick up some basics. Yet, for all its qualities, Britain’s largest retailer remains at the mercy of the country’s ongoing cost-of-living crisis. And right now it’s being hit harder than analysts predicted.

Its Booker wholesale division was the worst performer in Q1, as the numbers above show. This reflected tough year-on-year comparatives and the exit of a lower-margin contract.

Yet fears over Tesco’s UK trading are the main issue. This is the engine room of the firm’s operation, accounting for roughly three-quarters of revenues. Like-for-like sales grew 1.8% in Q1, which was exactly half a percentage point below what analysts were expecting.

No room for error

In terms of Tesco’s shares, the problem is that they look pricey from an historical perspective. At 448p per share, they trade on a forward price-to-earnings (P/E) ratio of 15 times. That’s above the 10-year average of 11-12.

That’s not outrageously expensive, sure. But any share that trades above value needs to regularly hit broker forecasts at a minimum. That’s clearly not happened with Tesco today, hence its share price fall.

The problem is the sales could remain under pressure in the months ahead, leading to further disappointing trading statements. If so, a sharp re-rating of Tesco’s shares can be expected.

What could go wrong?

One danger is that consumers continue feeling the pinch as inflationary pressures grow. In this climate, too, Tesco’s will have limited scope to pass rising costs onto customers, impacting margins.

Finally, the recovery of rivals in the famously competitive food retail segment could affect Tesco’s sales. As those analysts at RBC Capital also mention,

Market share gains have moderated in recent periods, and we expect this trend to continue given competitors in the UK are starting to stabilise their volume losses.

I certainly won’t be taking a risk with Tesco’s shares today. And especially given the FTSE firm’s high market valuation.

Should you invest £5,000 in Tesco Plc right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Tesco Plc made the list?

Royston Wild does not hold any positions in the companies mentioned.